Social Security is a bedrock program in the United States. Social Security is an entitlement program that pays millions of people an income each month.

This is part of a 4 part Social Security series.

Part 2 - Social Security: The Benefits

How Social Security Is Formulated

Social Security pays out each person’s PIA - Primary Insurance Amount.

PIA =

90% of AIME until bend point 1, plus

32% of AIME between bend points 1 & 2, plus

15% of AIME over bend point 2.

For 2021, this looks like:

90% of AIME on the first $996, plus

32% of AIME over $996 through $6,002, plus

15% of AIME over $6,002

As you can see, this gives a greater proportionate benefit to workers who were paid less and gives less to higher earners.

Bend points are updated each year and can be found here

AIME

Average indexed monthly earnings (AIME) is the primary determinant of the benefits that get paid out. It’s calculated by summarizing a worker’s highest 35 years of indexed earnings.

In simple terms, indexed earnings are all past earnings adjusted for inflation. Thus ensuring benefits rise similarly to the rise in the standard of living.

Further reading - Link to glossary of financial terms

Finding Your PIA, AIME, & Earnings Record

You can find all of this on the Social Security website. I highly suggest logging in and checking yours out. It takes about 5 minutes and pulls from public information to confirm your identity - don’t be alarmed by confirming past loans and addresses, http://www.ssa.gov/myaccount.

The Social Security Administration mails statements to eligible workers every 5 years starting age 25. These are mailed out to each qualified person. Happy birthday!

It’ll show your PIA/ benefits amount estimates for age 62, full retirement age (FRA), and age 70

Full Retirement Amount (FRA)

PIA is calculated based on your full retirement age. See the above chart to find yours. This age is critical for a few reasons beyond the obvious that we will dive into later.

The basic principle to know is that if you filing pre-FRA, benefits are reduced & if you file after FRA, benefits are increased.

Reduced Benefits & Delayed Retirement Credits

You can start claiming Social Security at age 62 and delay social security until age 70. There are benefits to waiting until FRA or even waiting until age 70.

Pre-FRA, your benefits are reduced for each month you filed early.

5/9ths of 1% per month for the first 36 months (6.66% per year), and

5/12ths of 1% for each additional month (5% per year)

After-FRA, your benefits are increased for each month you delay filing. This lasts until age 70.

These are Delayed Retirement Credits (DRC) of 2/3rds of 1% per month (8% per year).

How Are Benefits Taxed

Not all of Social Security is subject to tax. Up to 85% is subject to income tax for higher incomes.

You can find the tax bracket here each year.

For 2021:

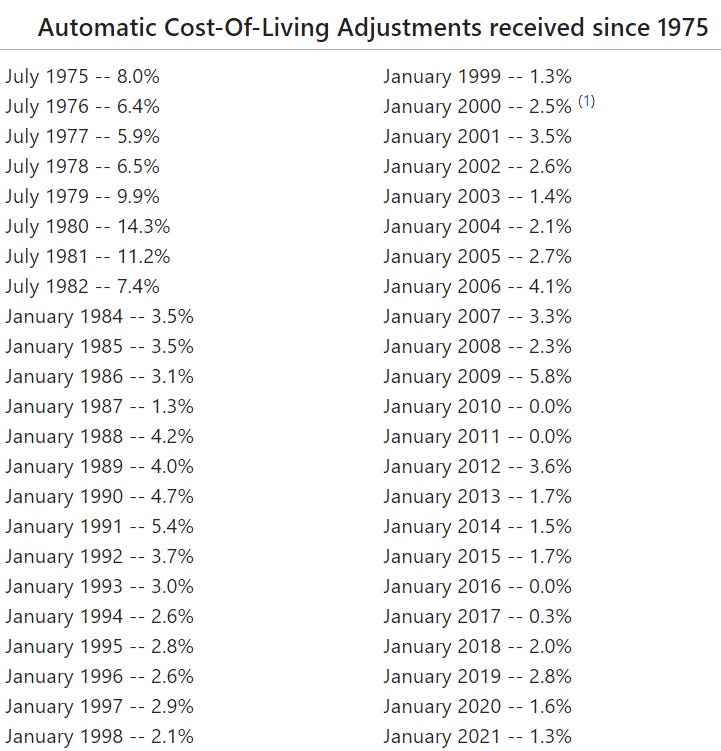

Cost of Living Adjustment (COLA

One key aspect of Social Security benefits over most pensions is that it has a COLA. Each year the benefits can be increased.

Good news for Social Security Recipients

Stephen Goss, SSA’s chief actuary, told the media that the COLA will be close to 6% for 2022 (Edit: 5.9% was the final COLA for 2022).

Did you enjoy this newsletter?

Share it! A referral is always the best compliment.